Green / Social / Sustainability Bonds

Increasingly, at least in the world of finance, we see an interest regarding Environmental, Social and Governance (ESG) topics - hence the term ESG finance or sustainable finance. What does that even mean? If a company issues a Green Bond, does that mean that it is inherently an ESG darling or that investors find that company to be a leader in ESG? In this article, we discuss what a Green Bond actually is and then discuss how exactly treasury & sustainability teams can go about structuring a Green Bond.

Breaking down Green, Social and Sustainability Bonds

Finance, unfortunately, is known to have distinct nomenclature and ESG finance is no different. To boil it down, Green and Social Bonds fund projects that have an environmental and social impact, respectively. Sustainability Bonds are instruments that encompass both environmental and social projects.

Environmental and social impact. That's still pretty broad right? How do issuers and investors determine what is acceptable or "market"? This is when the International Capital Markets Association (ICMA) comes into play. ICMA is a not-for-profit trade association that comprises members from investment and central banks, institutional investors, law firms, academic institutions and many more. Similar to other trade associations, a well-known example being the American Diabetes Association, ICMA's mission is to educate firms or individuals on market best practices and encourage capital markets participants to adhere to specific standards. For Green, Social and Sustainability Bonds, ICMA publishes voluntary guidelines for issuers to refer to. I'll link those guidelines and other relevant documents at the end of this article.

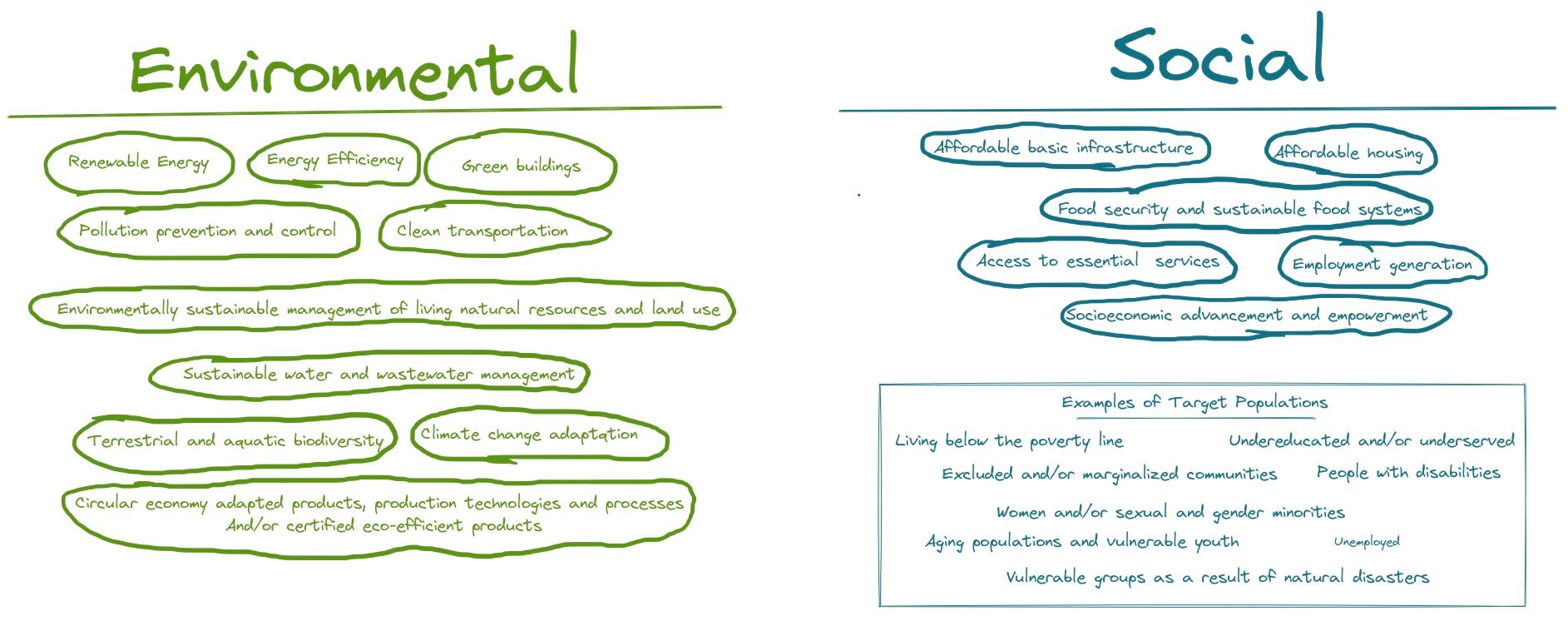

Green and Social Project Categories

Under the Green Bond Principles, updated as of June 2021, there are 10 eligible project categories that an issuer can choose from. Similarly, the Social Bond Principles details 6 categories, in addition to example target populations. What are target populations? Proceeds from a Social Bond typically tries to mitigate a particular social issue (e.g., hunger / access to food). The goal of having a target population is to encourage positive social outcomes for individuals that might be disproportionally and negatively effected by a social issue. Because the issuer commits to disbursing the net proceeds to green and/or social projects i.e., labels the dollars raised, market participants will use the term 'labeled instruments' to refer to these securities.

Within each Green and Social project category, issuers are able to further define which initiatives and/or expenditures fall under each one. Typically, companies would publish a standalone document or framework that details the project categories that could be utilized for an issuance. I'll link to a few examples at the bottom of this article. Some companies choose to make their framework as an extension of their corporate ESG reporting and pull out all the bells and whistles i.e., have the internal communications / graphics team vet and format the document to look like their annual Corporate Social Responsibility report, whereas, others might have a simplistic word document that details the components. From an execution and (in my experience thus far) an investor perspective, there isn't a preference for either approach, though it may be beneficial for companies to have more built out document if they'd like to use the ESG financing as a marketing or public relations exercise.

In my next article, I'll detail common components of a ESG Financing Framework for a labeled issuance i.e., for Green Bonds, Social Bonds and Sustainability Bonds.

Relevant Links:

Example frameworks:

- Alphabet / Google Sustainability Bond Framework

- Kellogg Sustability Bond Framework

- Walmart Green Financing Framework

#labeled